[Upside]

1. M&A Synergies (operational, distribution and logistical synergies) resulted in improvement in profit margin. The cost synergies should reflect better than current valuation in the future.

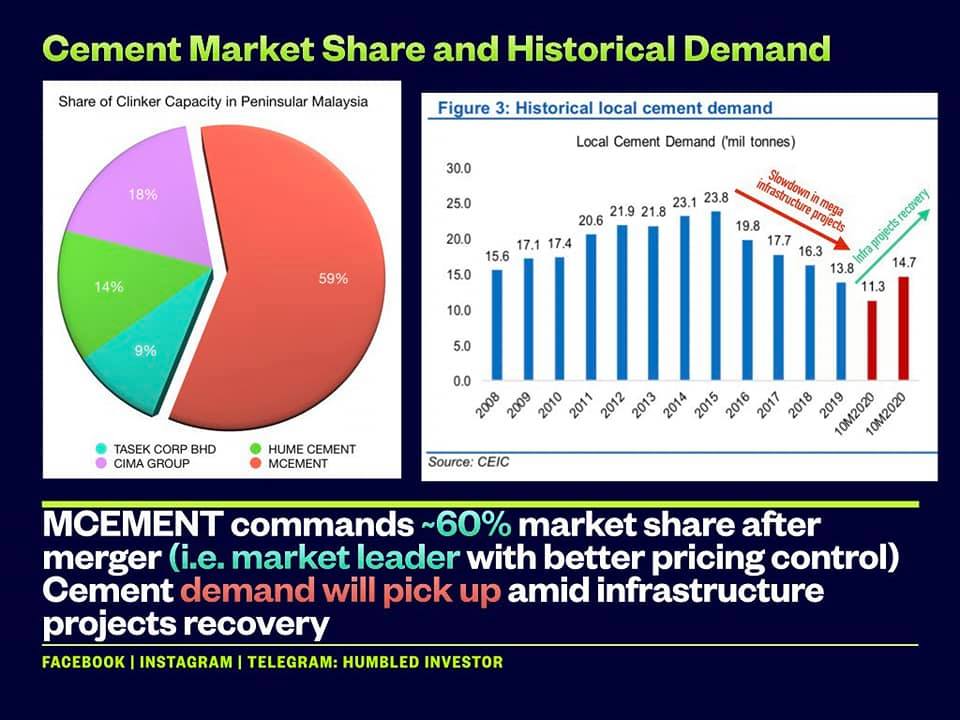

2. Economy recovery would revive property and construction sectors which will then increase demand for cement.

3. Cement has a short shelf life of 3 months. Better inventory management will help to accomodate with incoming demand from the revival of various big infra projects.

4. Cement price will be better managed after sector consolidation (with MCEMENT remains as the market leader with 60% market share).

5. Technical chart wise, the 20-years chart showed a huge support at RM1.80 level and YTL acquired Lafarge (nka MCEMENT) at RM3.75. MCEMENT currently trading at RM2.36.

6. Potential to turn net profit in the next few quarters.

[Downside]

1. Demand remains sluggish if MCO continues

with further delay in property/infrastructure projects

with further delay in property/infrastructure projects

2. Coal price has increased from 10-year low of RM210/MT to RM350/MT. However, MCEMENT might be able to transfer the increase in production costs to customers as MCEMENT now has better bargaining power against its customers after sector consolidation.

3. Market risk and volatility risk due to low public shareholding spread at 22.95% (excluding ASB).

4. Huge amount goodwill contributing 35% of total assets which are subject to annual impairment review. However the risk of further impairment is relatively low. This is because the goodwill arising from the acquistion of Lafarge Aggregates back in 2004 amounting to RM9mil has been impaired downwards to RM1.4mil as of June 2020 (-85% impairment) due to the lack of synergies to the existing business.

If you want to learn more, feel free to join us at:

💥Telegram Group:

https://t.me/humbledinvestordiscussion

💥Instagram:

https://www.instagram.com/humbledinvestor/

💥Trading Platform:

https://app.eventure.com.my/f216113b

_________________________________________________________________

All information provided here should be treated for informational purposes only. It is solely reflecting author's personal views and the author should not be held liable for any actions taken in reliance on information contained herein.

No buy call. No sell call. No bullshit. Only content.

If you think the article / information is useful to you, you can <SHARE> this article and support us by <LIKE> and <FOLLOW> our Facebook page "Humbled Investor". Thank you so much for supporting.